If Private Equity Can’t Model Five Years Out, How Can a Sixteen-Year-Old?

Yesterday, I read this Axios piece by Dan Primack —”AI creates a mess for private equity”—and it sent me down a rabbit hole I haven’t been able to climb out of.

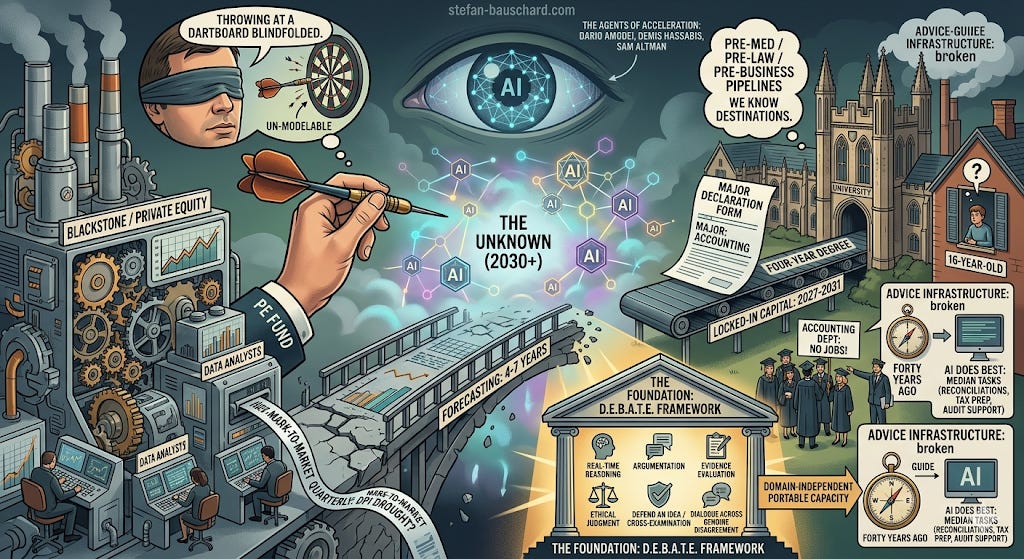

Primack’s argument is straightforward: Private equity, which is a medium-term asset class that typically holds portfolio companies for 4-7 years and then exits the investment, is struggling because AI is making it too difficult to predict what the economic value of any line of business, let alone a specific company, might be worth in 4-7 years. Basically, when a PE firm buys a company today and tries to project what someone will pay for it in 2030+, they are—in the words of one veteran Primack quoted—throwing at a dartboard blindfolded.

Read that again. The most sophisticated capital allocators on earth—people who employ armies of analysts, who can pay for any consultant, who have direct relationships with the AI labs themselves—are openly admitting they cannot model what the world looks like in 4 years.

And then I thought about the sixteen-year-old in high school

The bet we ask teenagers to make

Currently, in May 2026, a junior in high school is being asked to seriously consider what they want to major in. They’ll apply to college next fall. They’ll start their freshman year in 2027. They’ll graduate, if all goes well, in 2031.

That’s a five-year forecast. One year longer than the PE hold period that the industry is now describing as a “material weakness.” Two years longer than the window Primack’s sources call un-modelable.

We are asking sixteen-year-olds to make a more confident forecast about the labor market than Blackstone is willing to make about its own portfolio.

And it gets worse, because PE has tools the student doesn’t:

A PE firm holds twenty-plus companies. A student bets on one major.

A PE firm can write down a loss and redeploy capital. A student who picks wrong has spent four years and—if they borrowed—six figures of debt on a credential the market has discounted.

A PE firm marks to market quarterly. Universities don’t mark anything. The accounting major whose graduates can’t get jobs in 2029 will keep enrolling students in 2030.

A PE firm has analysts covering frontier AI capabilities full-time. The student has a guidance counselor whose advice infrastructure was calibrated to the 1990s labor market.

The PE industry, looking at a three-and-a-half-year horizon, is openly telling the financial press that the modeling has become impossible. The education industry, looking at a five-to-six-year horizon, is still handing out major declaration forms and pretending the math works.

Why this is worse than the PE problem

Primack frames the PE issue as a temporary embarrassment that will be partly absorbed by Q1 markdowns and renegotiated debt. The industry’s long-term nature, he writes, “always one of its greatest strengths, is becoming a material weakness.”

The same sentence describes higher education almost perfectly. Substitute “credential” for “portfolio company,” “graduating cohort” for “exit multiple,” and “tenure system” for “fund structure,” and the analysis ports cleanly. The four-year degree—long sold as the patient, durable bet—is the educational equivalent of the seven-year hold. Both rest on the assumption that you can lock in capital today against a stable future. Both assumptions are eroding for the same underlying reason.

But the cost falls in a different place.

When PE gets the model wrong, the loss is borne by limited partners—pension funds, endowments, sovereign wealth funds. These are diversified institutions. The pension can absorb a bad vintage. The endowment can offset a write-down. The sovereign wealth fund can wait it out.

When a student gets the bet wrong, there is no portfolio. There is one life, four years, the opportunity cost of those years, and—often—debt that follows them for decades. The “exit multiple” they’re trying to model is their own first job. There is no diversification. There is no patient capital cushion. There is just the kid.

The advice infrastructure is broken

Here’s what I keep coming back to. The people advising students—guidance counselors, parents, college admissions officers, the BLS Occupational Outlook Handbook, the salary projection websites, the “best majors for 2026” articles—are extrapolating from historical patterns. When a parent tells their kid to go into accounting because it’s stable, they’re drawing on forty years of accountants having stable careers. They aren’t pricing in that the median accounting task—reconciliations, tax preparation, audit support, financial statement analysis—is precisely what current AI does best.

The advice sounds prudent. The advice may be catastrophic. And the people giving it have no way to know which.

This isn’t a failure of intelligence or care on the part of counselors and parents. It’s a structural problem. The advice infrastructure was built for a slow-changing world. The world is no longer slow-changing. Even Primack’s PE veterans, with all their resources, can’t see three and a half years out. A guidance counselor with a caseload of one hundred students cannot be expected to do what Blackstone cannot do.

The institutional response will be too slow

Here’s the part that should make every parent of a high schooler pay attention. Primack’s piece notes that PE will continue making investments anyway, because limited partners keep allocating dry powder despite the DPI drought. The capital has to go somewhere. The funds were raised. The fees must be earned.

Universities are in the same position, only more so. Tenure, accreditation cycles, facilities debt, administrative overhead, and the four-year program structure all create momentum that prevents adaptation. A computer science department whose graduates struggle to find work in 2029 will not shut down. It will keep enrolling students in 2030, 2031, 2032, because the institutional machinery requires it. The university essentially cannot acknowledge in real-time that its product may be losing value, because acknowledging it would collapse the enrollment that funds the institution.

PE will probably take five to ten years to fully reckon with the modeling problem, because the funds raised in 2023–2025 still need to be deployed. Education will take fifteen to twenty years, because tenure and accreditation move slower than capital markets. Which means the students currently in high school will make their decisions inside an institutional framework that will not adjust in time to help them. The advice they get will be wrong. The credentials they pursue may be devalued. And the institutions providing those credentials will keep operating as if nothing has changed.

My gripe with the current educational system

Here’s what actually keeps me up at night. It isn’t that we don’t know which professions will survive AI. Nobody knows that. The PE veterans don’t know it. Dario Amodei doesn’t know it. Demis Hassabis doesn’t know it. Not knowing isn’t the problem.

The problem is that the educational system refuses to admit it doesn’t know.

Walk into almost any high school in America, and you’ll find the same machinery still running: course catalogs organized around traditional career pathways, guidance counselors steering students toward “stable” professions, AP tracks designed to feed pre-med and pre-law and pre-business pipelines, college admissions essays asking sixteen-year-olds to articulate “what you want to be.” The whole apparatus is calibrated as if we’re confidently sending students down particular career paths toward known destinations. We’re not. We’re sending them toward destinations that may not exist when they arrive, and the system is pretending otherwise.

Look at where AI has already gone. It came for the coders first—and that one stings, because coding was supposed to be the safe bet, the future-proof pathway, the thing every guidance counselor in America was telling kids to pursue five years ago. Now it’s coming for financial services. It’s well into the legal profession—document review, contract analysis, legal research, the work that used to fill the first three years of a young attorney’s career. It’s making serious inroads into research itself, which is a strange thing to watch, because research is what professors do, and professors are the ones training the next generation for the professions AI is now eating. It’s pushing into medicine—diagnostic imaging, differential diagnosis, treatment planning, the cognitive core of what doctors actually do.

And AI is just getting started. We are, at most, four years into the generative AI era. The capabilities curve is still bending sharply upward. Anyone who tells you with confidence which professions will be intact in 2031 is doing the same thing Primack’s PE sources are doing—except without the self-awareness to admit they’re guessing.

We cannot, with a straight face, tell students that any profession is sacred. We cannot promise them that medicine will look like medicine, or that law will look like law, or that finance will look like finance. We don’t know. Some will survive in recognizable form. Some will be transformed beyond recognition. Some will mostly disappear. We don’t know which is which, and pretending we do is a kind of malpractice.

But here’s the thing—there is one thing we do know. We know that the fundamental human capacities will matter no matter which professions emerge on the other side. Real-time reasoning. Argumentation. Evidence evaluation. Ethical judgment under pressure. The ability to defend an idea when an intelligent person is pushing back across the table. The ability to change your mind when the pushback is good. Dialogue across genuine disagreement. These are the things that don’t get commoditized when the labor market gets reshuffled. These are the things that matter in every possible future configuration, because they’re the capacities that let a human direct AI rather than be directed by it.

This is the one thing we know. And what does the educational system do with the one thing we know?

It often treats it as an extracurricular. It funds it as a club. Speech and debate—the single most direct training ground for exactly the capacities that will survive AI disruption—is offered at most schools as an after-school activity for the kids who happen to be interested, run by a teacher who is doing it on top of a full or nearly full course load, and a limited budget. Meanwhile, the resources flow to the coursework training students for the careers we cannot promise will exist.

That is my gripe. We are lowballing the only thing we know is durable, while we keep dressing up the things we don’t know in the costume of certainty. We treat the AI-resilient capacities as enrichment for the interested, when they should be the currency of the emerging AGI world. Every student should be doing this work. Every student. Not as a club. As the core.

The PE industry is at least having the conversation. They’re saying out loud that the modeling is broken, that the long-term bets they’ve always made don’t pencil out the way they used to. The educational system isn’t even at that stage. It’s still printing the same course catalogs, still routing students into the same pipelines, still telling sixteen-year-olds to pick a major and plan a career as if the next decade will resemble the last one.

It won’t. And we owe these kids better than the pretense that it will.

So what do we tell the sixteen-year-old?

I don’t think the answer is “don’t go to college” or “skip the major.” That’s the wrong frame, and it’s not what I’d tell my own students. The answer is that the entire pick-a-major-as-life-bet model is itself the obsolete asset. It’s not that students are picking the wrong majors. It’s that the framework of treating a major as a five-year forecast on labor market value was always fragile, and AI has now exposed the fragility.

The replacement isn’t a smarter major. It’s a different theory of what education is for.

If you cannot reliably forecast which specific knowledge bundles will be valuable in 2031, you have to bet on capacities that survive whatever specific economic configuration emerges. Real-time reasoning under pressure. Evidence evaluation. Adversarial argumentation with a human across the table. Ethical judgment when no rule covers the case. The ability to defend an idea under cross-examination and to change your mind when the cross-examination is good. Dialogue across genuine disagreement.

These are the things I’ve been writing about as the D.E.B.A.T.E. framework, and I keep coming back to them, not because debate is my hammer and everything looks like a nail, but because these capacities are domain-independent. They don’t depend on guessing right about which industries will exist in 2031. A student who can think well, evaluate evidence, and defend ideas under cross-examination has a portable capacity that survives any specific economic configuration. A student who has memorized the 2026 marketing curriculum does not.

The Axios piece is, on its face, about private equity. But the deeper story is about every institution that asks people to lock in capital today against a future that nobody can model. PE is reckoning with this in real time. So is higher education—it just doesn’t know it yet, or it knows and can’t say so out loud.